DAYBREAK OIL AND GAS, INC.

601 W. Main Avenue, 1101 N. Argonne Rd.

Suite 1012A 211

Spokane Valley, WA 9920199212

June 10, 2010April 21, 2022

TO OUR SHAREHOLDERS:

TO OUR SHAREHOLDERS:

We cordiallyare pleased to provide you notice of, and to invite you to attend, the Annuala Special Meeting of the Shareholders (the “Annual“Special Meeting”) of Daybreak Oil and Gas, Inc., a Washington corporation (“Daybreak”, the “Company,” “we,” “our” or “us”), as called by the Board of Directors to be held on Thursday, July 22, 2010,May 20, 2022 at 10:00 AM (PDT)a.m., local time, at 601 W. Main Avenue, Spokane, Washington 99201.4800 Bee Caves Rd., Suite 100, Austin, Texas 78746 (subject to postponement(s) or adjournment(s) thereof).

The attached Notice of AnnualSpecial Meeting of Shareholders and proxy statement provide more information concerning the matters to be considered at the AnnualSpecial Meeting. We do not expect to transact any other business at the Special Meeting.

Pursuant

Daybreak has faced the challenges of declining oil prices (historically) and the lack of outside financing for several years. We have been working steadily to rules promulgatedminimize overhead and unnecessary expenditures, simplify our share structure, and position the Company for a strategic turnaround transaction. We are excited to let you know that we have simplified and optimized the Company, and have entered into an agreement for a proposed transaction that we believe will position Daybreak for future success.

This transaction involves us issuing Company common stock to acquire another California oil and gas exploration and production company. You are not being asked to sell or exchange your shares and you will keep your Daybreak shares.

On October 20, 2021, and subsequently amended on February 22, 2022, we entered into an Equity Exchange Agreement (as amended, the “Exchange Agreement”) by and between Daybreak, Reabold California LLC, a California limited liability company (“Reabold”), and Gaelic Resources Ltd., a private company incorporated in the U.S. SecuritiesIsle of Man and the 100% owner of Reabold (“Gaelic”), pursuant to which the parties propose for (i) Daybreak to acquire 100% ownership of Reabold, in exchange for (ii) Daybreak issuing 160,964,489 shares of its common stock, par value $0.001 (“Common Stock”) to Gaelic (the “Exchange Shares”), which will result in Reabold becoming a wholly-owned subsidiary of Daybreak named “Reabold California, LLC” and Gaelic becoming the owner of the Exchange Commission,Shares and a major shareholder of Daybreak (the foregoing transaction and the transactions contemplated thereby, the “Equity Exchange”).

In connection with the Equity Exchange, and as conditions to closing the Equity Exchange, we also propose to:

| (a) | Amend and restate our Amended and Restated Articles of Incorporation by adopting the Second Amended and Restated Articles of Incorporation of the Company to (i) increase the number of total authorized shares of Common Stock to 500,000,000 to provide enough shares to accomplish the transactions contemplated by the Equity Exchange and conducted in anticipation of the Equity Exchange, complete the Capital Raise (defined below under (d)), and have shares available for other potential future issuances, and (ii) allow a majority share vote to approve transactions where a higher vote is provided by the Washington Business Corporation Act; |

| (b) | Nominate a nominee selected by Reabold to the Daybreak Board of Directors, such nominee, if elected, to join the board effective as of the closing of the Equity Exchange; |

| (c) | Enter into a voting agreement by and among Daybreak, Gaelic and the Company’s Chairman and Chief Executive Officer, James F. Westmoreland, where, on the terms therein, Daybreak and the |

| shareholder parties thereto agree to nominate a person designated by Gaelic and a person designated by James F. Westmoreland to Daybreak’s Board of Directors, and the parties thereto agree to vote their shares in favor of such candidates (the “Voting Agreement”); |

| (d) | Enter into agreements to sell a minimum of $2,500,000 of shares of Daybreak’s Common Stock, and a minimum of 125,000,000 shares of Common Stock, to one or more investors in a private placement expected to close promptly following the closing of the Equity Exchange (the “Capital Raise”), with the proceeds of the Capital Raise to be used to repay in full the Company’s line of credit with UBS Bank and for drilling and exploration activities and other working capital purposes; |

| (e) | Enter into a registration rights agreement between Daybreak and the purchasers of common stock pursuant to the Capital Raise giving such purchasers rights to demand or participate in registration of Common Stock held by them on the terms contained therein; |

| (f) | Effective upon the closing of the Equity Exchange, appoint Integrity Management Solutions, Inc. (“Integrity”), a California operating company that provides engineering and contract operating services for Reabold California LLC’s oil and gas properties. Integrity has been providing these services for the Reabold properties since July, 2018, as contract operator of Reabold’s oil and gas license interests for a minimum of a one (1) year period. |

| (g) | Effective upon the closing of the Equity Exchange, enter into indemnification agreements between Company and its directors. |

Further, in connection with the Equity Exchange, and as conditions to closing the Equity Exchange, we have already taken the following steps to simplify the Company’s share structure and eliminate indebtedness:

| (h) | Converted all shares of Series A Preferred Stock of the Company to Common Stock by approval of the holders of a majority of the shares of Series A Preferred Stock (the “Series A Conversion”); |

| (i) | Converted $1,837,101 of related party liabilities of Daybreak into Common Stock of the Company (the “Related Party Debt Conversion”), including all accrued and unpaid salary and fees of our named executive officers, certain other employees, and directors. |

| (j) | The Company’s President and Chief Executive Officer forgave $43,192 in deferred salary payments, net of related taxes and expense reimbursements. |

The Daybreak Board of Directors believes the Equity Exchange and the transactions contemplated thereby and described above, are the best path forward for the Company and are in the best interest of the shareholders.

At the Special Meeting, we will be seeking the shareholder approvals necessary to complete the Equity Exchange. Specifically, we will be asking you to, among other things:

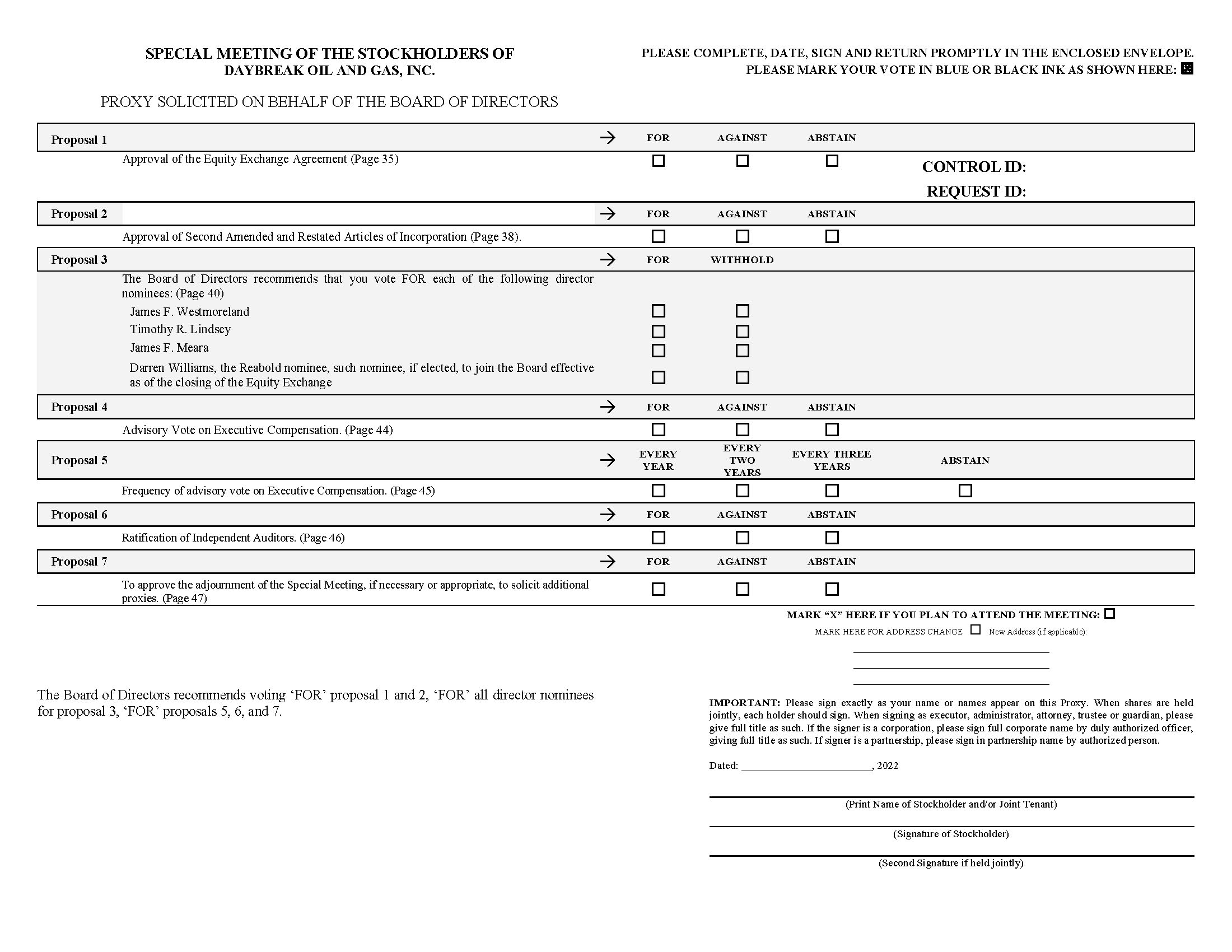

| 1. | Consider and vote upon a proposal to approve the Equity Exchange and the issuance of the Exchange Shares pursuant to the terms of the Exchange Agreement. |

| 2. | Consider and vote upon a proposal to approve amending and restating our Amended and Restated Articles of Incorporation to (i) increase the number of total authorized shares of Common Stock to 500,000,000 to provide enough shares to accomplish the transactions contemplated by the Equity Exchange and conducted in anticipation of the Equity Exchange, complete the Capital Raise, and have shares available for other potential future issuances, (ii) eliminate the designation of the Series A Convertible Preferred Stock and (iii) allow a majority share vote to approve transactions where a higher vote is provided by the Washington Business Corporation Act. |

| 3. | Consider and vote upon a proposal to elect the following four (4) directors nominated by our Board of Directors to the Daybreak Board of Directors, to serve until the Company’s next Annual Meeting of Shareholders, or until their earlier, death, resignation or removal: |

Further, as we have previously disclosed, due to our limited financial resources, the Company has not held an annual meeting of our shareholders since 2010. Therefore, at the Special Meeting, in addition to matters involving the Equity Exchange and the election of directors, we will also providing accessbe asking you to consider the following matters:

| 4. | Consider and vote, on an advisory basis, on the compensation of our Named Executive Officers. |

| 5. | Consider and vote, on an advisory basis, on the frequency of future advisory votes regarding compensation. |

| 6. | Ratify the appointment of our independent registered public accountant for the fiscal year ended February 28, 2022. |

Since our proxy materials overare being furnished fewer than 40 days prior to the Internet. As a result,shareholder meeting date, we are mailing to most of our shareholders a Notice of Internet Availability of Proxy Materials (“Notice”) instead of a paper copy of this proxy statement, a proxy card, a letter to shareholders from our President and Chief Executive Officer, and our annual report on Form 10-K for the fiscal year ended February 28, 2010. The Notice contains instructions on how2021. Pursuant to rules promulgated by the U.S. Securities and Exchange Commission, we are also providing access those documentsto our proxy materials over the Internet, as well as instructions on how to request a paper copy of our proxy materials. All shareholders who do not receive a Notice should receive a paper copy of the proxy materials by mail. We believe that the Notice process represents a more direct mechanism for disseminating information, and will reduce both the environmental impact and associated costs of producing and delivering the proxy materials.Internet.

As owners of Daybreak Oil and Gas, Inc. stock, your

Your vote is important. Whether or notEnclosed is a proxy that will entitle you planto vote your shares on the matters presented at the Special Meeting, even if you are unable to attend the Annual Meeting, we hope that you will vote as soon as possible.in person. You may vote by proxy over the Internet or by telephone using the instructions on the Notice, or, if you received a paper copy of the proxy card, by signingyou can mark the proxy to indicate your vote, date and returningsign the proxy and return it in the postage-paidenclosed envelope provided. You may also attend and voteas soon as possible for receipt prior to the Special Meeting. Regardless of the number of shares you own; please be sure you are represented at the AnnualSpecial Meeting either by attending in person or by returning your proxy or voting on the internet as soon as possible.

Even if you plan to attend the Special Meeting, we request that you submit a proxy by following the instructions on your proxy card as soon as possible and thus ensure that your shares will be represented at the Special Meeting if you are unable to attend.

We are excited about the opportunities for the Company’s future, and our Board of Directors recommends that you vote your shares in favor of the proposals to be presented at the Special Meeting.

On behalf of our Board of Directors, thank you for your continued interest in Daybreak Oil and Gas, Inc. We look forward to seeing you on July 22nd.May 20, 2022.

Sincerely,

| Sincerely, | |

| /s/ James F. Westmoreland | |

| James F. Westmoreland | |

| Chairman of the Board of Directors |

/s/ Dale B. Lavigne

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this proxy statement. Any representation to the contrary is a criminal offense.

Dale B. LavigneThe accompanying proxy statement is dated April 21, 2022, and is first being mailed to Daybreak shareholders on or about April 21, 2022.

Chairman of the Board of Directors

DAYBREAK OIL AND GAS, INC.

1101 N. Argonne Rd. Suite A 211

Spokane Valley, WA 99212

______________

N601 W. Main Avenue, Suite 1012

Spokane, WA 99201

NOTICEOTICE OF ANNUAL MEETINGSPECIAL MEETING OF SHAREHOLDERSSHAREHOLDERS

July 22, 2010April 21, 2022

______________

NOTICE IS HEREBY GIVENNotice Is Hereby Given that the 2010 Annuala Special Meeting of Shareholders of Daybreak Oil and Gas, Inc. will be held at 10:00 AM (PDT)a.m., local time, at 4800 Bee Caves Rd., Suite 100, Austin, Texas 78746, on Thursday, July 22, 2010, at 601 W. Main Avenue, Spokane, Washington 99201,April 21, 2022, to consider and act upon the following matters:

1. | To consider and vote upon a proposal to approve the Equity Exchange as contemplated by the Equity Exchange Agreement (as amended, the “Exchange Agreement”) by and between Daybreak, Reabold California LLC, a California limited liability company (“Reabold”), and Gaelic Resources Ltd., a private company incorporated in the Isle of Man and the 100% owner of Reabold (“Gaelic”), pursuant to which the parties propose for a plan of share exchange whereby (i) Gaelic will irrevocably assign and transfer all of its ownership interests in Reabold to Daybreak, and (ii) Daybreak will issue 160,964,489 shares of its common stock to Gaelic (the “Exchange Shares”), which will result in Reabold becoming a wholly-owned subsidiary of Daybreak named “Reabold California, LLC” and Gaelic becoming the owner of Exchange Shares (the foregoing transaction, the “Equity Exchange”), on the terms and subject to the conditions set forth in the Exchange Agreement; A copy of the Exchange Agreement, and amendment is attached as Annex A to the accompanying proxy statement. |

| 2. | To consider and vote upon a proposal to approve amending and restating the Company’s Amended and Restated Articles of Incorporation by adopting the Company’s Second Amended and Restated Articles of Incorporation to increase the number of total authorized shares of Daybreak Common Stock to 500,000,000 to provide enough shares to accomplish the transactions contemplated by the Equity Exchange and conducted in anticipation of the Equity Exchange, complete the Capital Raise, and have shares available for other potential future issuances; eliminate the designation of the Series A Convertible Preferred Stock; and allow a majority share vote to approve transactions where a higher vote is provided by the Washington Business Corporation Act. A copy of the Second Amended and Restated Articles is attached as Annex B to the accompanying proxy statement. |

| 3. | To consider and vote upon a proposal to elect |

| 4. | To consider and vote, on an advisory basis, on the compensation of our Named Executive Officers, as disclosed in |

| 5. | To consider and vote, on an advisory basis, on the frequency of future advisory votes regarding compensation of our Named Executive Officers; |

| To ratify our appointment of MaloneBailey, LLP as our independent registered public accountants for the fiscal year ending February 28, |

| To consider |

We have not received notice of other matters that may be properly presented at the AnnualSpecial Meeting or any adjournment or postponement thereof.

Only shareholders of record of the Company’s common stock and Series A Convertible Preferred stock at the close of business on May 27, 2010March 22, 2022 are entitled to notice of and to vote at the AnnualSpecial Meeting.

Please take the time to vote by following the Internet or telephone voting instructions provided. If you received a paper copy of the proxy card, you may also vote by completing and mailing the proxy card in the postage-prepaid envelope provided for your convenience.

We recommend that you complete and return a proxy even if you plan to attend the AnnualSpecial Meeting; you will be free to revoke your proxy and vote in person at the meeting if you wish. If you wish to vote your shares at the meeting, the inspector of election will be available to record your vote at the meeting site beginning at 9:30 AM (PDT)a.m. on the date of the meeting.

By Order of the Board of Directors,

/s/ Karol L. Adams

Karol L. Adams

Corporate Secretary

Spokane, Washington

June 10, 2010

TABLETHE DAYBREAK BOARD OF CONTENTSDIRECTORS HAS DETERMINED AND BELIEVES THAT EACH OF THE PROPOSALS OUTLINED ABOVE IS ADVISABLE TO, AND IN THE BEST INTERESTS OF, DAYBREAK AND ITS SHAREHOLDERS AND HAS APPROVED EACH PROPOSAL. THE DAYBREAK BOARD OF DIRECTORS UNANIMOUSLY RECOMMENDS THAT DAYBREAK SHAREHOLDERS VOTE “FOR” PROPOSAL NOS. 1 THROUGH 7.

| By Order of the Board of Directors, | |

| /s/ Karol L. Adams | |

| Karol L. Adams | |

| Corporate Secretary |

Spokane Valley, Washington

April 21, 2022

TABLE OF CONTENTS

| |

Consideration of Nominees and Qualifications for Nominations to the Board of Directors |

|

| |

| |

|

Communications Between Interested Parties and the Board of Directors |

|

| |

| |

| |

| |

| |

| |

| |

|

|

|

|

| |

|

|

|

|

|

|

|

|

| |

| |

|

|

| 64 | |

| General Discussion of Executive Compensation | 64 |

| Summary Compensation Table |

|

|

|

| |

| 66 | |

| Payments Upon Termination or Change of Control | 66 |

| Pension Plan Benefits | 66 |

| Deductibility of Compensation | 66 |

| Stock Compensation Expense | 66 |

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

|

| 69 |

| SECTION 16(A) BENEFICIAL OWNERSHIP REPORTING COMPLIANCE |

|

| 70 | |

| SHAREHOLDER PROPOSALS FOR |

|

| INFORMATION INCORPORATED BY REFERENCE | 71 |

DAYBREAK OIL AND GAS, INC.

601 W. Main Avenue,1101 N. Argonne Rd. Suite 1012A 211

Spokane Valley, WA 9920199212

____________

PROXY STATEMENT

FOR

ANNUALSPECIAL MEETING OF SHAREHOLDERS

To Be Held May 20, 2022

____________

To Be Held July 22, 2010

GENERAL INFORMATION ABOUT THE MEETING, VOTING AND PROXIES

Date, Time and Place of Meeting

The Board of Directors (the “Board”) of Daybreak Oil and Gas, Inc., a Washington corporation (the “Company” or “Daybreak”), is soliciting your proxy to be voted at the AnnualSpecial Meeting of Shareholders (the “Annual“Special Meeting”) to be held aton May 20, 2022 10:00 AM (PDT)a.m., on Thursday, July 22, 2010,local time, at our corporate headquarters at 601 W. Main Avenue, Spokane, Washington 99201,4800 Bee Caves Rd., Suite 100, Austin, Texas 78746, for the purposes set forth in the accompanying Notice of AnnualSpecial Meeting of Shareholders, and at any adjournments of the AnnualSpecial Meeting. The proxy materials, including this proxy statement, proxy card or voting instructions, a letter to shareholders from our President and Chief Executive Officer, and our annual report on Form 10-K for the fiscal year ended February 28, 20102021 are first being distributed and made available to Shareholders on or about June 11, 2010.April 21, 2022. You should carefully read the entire proxy statement and the additional documents referred to in this proxy statement for a more complete understanding of the matters being considered at the special meeting. In this Proxy Statement,proxy statement, unless the context requires otherwise, when we refer to “we,” “us,” “our” or the “Company,” we are describing Daybreak Oil and Gas, Inc.

At the AnnualSpecial Meeting, we will ask our shareholders to consider and act upon the following matters:

| 1. | To consider and vote upon a proposal to approve the Equity Exchange as contemplated by the Equity Exchange Agreement, (as amended, the “Exchange Agreement”) by and between Daybreak, Reabold California LLC, a California limited liability company (“Reabold”), and Gaelic Resources Ltd., a private company incorporated in the Isle of Man and the 100% owner of Reabold (“Gaelic”), pursuant to which the parties propose for a plan of share exchange whereby (i) Gaelic will irrevocably assign and transfer all of its ownership interests in Reabold to Daybreak, and (ii) Daybreak will issue 160,964,489 shares of its common stock to Gaelic (the “Exchange Shares”), which will result in Reabold becoming a wholly-owned subsidiary of Daybreak named “Reabold California, LLC” and Gaelic becoming the owner of Exchange Shares (the foregoing transaction, the “Equity Exchange”), on the terms and subject to the conditions set forth in the Exchange Agreement; |

| To consider and vote upon a proposal to approve amending and restating the Company’s Amended and Restated Articles of Incorporation to increase the number of total authorized shares of Daybreak Common Stock to 500,000,000 to provide enough shares to accomplish the transactions contemplated by the Equity Exchange and conducted in anticipation of the Equity Exchange, complete the Capital Raise, and have shares available for other potential future issuances; eliminate the designation of the Series A Convertible Preferred Stock; and allow a majority share vote to approve transactions where a higher vote is provided by the Washington Business Corporation Act; |

-1-

| 3. | To consider and vote upon a proposal to elect |

| 4. | To consider and |

| To consider and vote, on an advisory basis, on the frequency of future advisory votes regarding compensation of our Named Executive Officers; |

| 6. | To ratify our appointment of MaloneBailey, LLP as our independent registered public accountants for the fiscal year ending February 28, |

| To consider |

Recommendations of the Board of Directors

Our Board of Directors unanimously recommends athat Daybreak Shareholders vote “FOR” the election of eachproposal to approve the Equity Exchange on the terms set forth in the Equity Exchange Agreement and “FOR” all the other proposals to be considered at the special meeting. For a description of the six director nominees, and “FOR”reasons considered by the ratificationBoard in deciding to recommend the adoption of the appointmentEquity Exchange Agreement, see the section entitled “The Equity Exchange Agreement (Proposal 1) — Recommendation of MaloneBailey, LLP as Daybreak’s independent registered public accountantsthe Board and Reasons for the Exchange Agreement” beginning on page 35 of this proxy statement.

Notice of Mailing of Proxy Materials

Since our proxy materials are being furnished fewer than 40 days prior to the shareholder meeting date, we are mailing our shareholders a paper copy of this proxy statement, a proxy card, a letter to shareholders from our President and Chief Executive Officer, and our annual report on Form 10-K for the fiscal year endingended February 28, 2011.

Information About the Notice of Internet Availability of Proxy Materials

In accordance with2021. Pursuant to rules and regulations adoptedpromulgated by the U.S. Securities and Exchange Commission (the “SEC”), we are also providing our shareholders access to our proxy materials onover the Internet. Accordingly, a Notice of Internet Availability of Proxy Materials (“Notice”) will be mailed to most of our shareholders on or about June 11, 2010. Shareholders will have the ability to access the proxy materials on a web site referred to in the Notice or request a printed set or e-mail copy of the proxy materials to be sent to them by following the instructions in the Notice.

- 1 -

Daybreak is providing certain shareholders, including those who have previously requested to receive paper copies of the proxy materials, with paper copies of the proxy materials instead of a Notice. If you would like to reduce the costs incurred by Daybreak in mailing proxy materials, you can consent to receive all future proxy statements, proxy cards and annual reports electronically via e-mail or the Internet. To sign up for electronic delivery, please follow the instructions provided with your proxy materials and on your proxy card or voting instruction card to vote using the Internet. When prompted, indicate that you agree to receive or access shareholder communications electronically in the future. Your election to receive proxy materials by e-mail or printed form will remain in effect until you terminate it.

Notice of Internet Availability of Proxy Materials

Daybreak is pleased to be using the SEC rule that allows companies to furnish their proxy materials over the Internet. As a result, Daybreak is mailing to many of its shareholders a Notice about the Internet availability of the proxy materials instead of mailing a paper copy of the proxy materials. All shareholders receiving the Notice will have the ability to access the proxy materials over the Internet and request to receive a paper copy of the proxy materials by mail. Instructions on how to access the proxy materials over the Internet or to request a paper copy may be found on the Notice.

Important Notice Regarding the Internet Availability of Proxy Materials for the AnnualUpcoming Special Meeting of Shareholders to be Held on July 22, 2010:

This Proxy Statement,proxy statement, letter to shareholders from our President and Chief Executive Officer, and 20102021 Annual Report on Form 10-K are available at: on our website at www.proxyvote.comwww.daybreakoilandgas.com., from commercial document retrieval services and on the website maintained by the SEC at http://www.sec.gov.

| -2- |

This solicitation of proxies is by Daybreak, the registrant.

In addition to the solicitation of proxies by use of this Proxy Statement,proxy statement, our directors, officers and employees may solicit the return of proxies by mail, personal interview, telephone or facsimile. We will not pay additional compensation to our directors, officers or employees for their solicitation efforts, but we will reimburse them for any out–of–pocket expenses they incur in their solicitation efforts. We will request that brokerage houses and other custodians, nominees and fiduciaries forward solicitation materials to the beneficial owners of stock registered in their names. We will ask brokerage houses and other custodians and nominees whether other persons are beneficial owners of Daybreak common stock. If so, we will supply them with additional copies of the proxy materials for distribution to the beneficial owners. We will also reimburse banks, nominees, fiduciaries, brokers and other custodians for their costs of sending the proxy materials to the beneficial owners of Daybreak common stock.

We will bear all costs of preparing, printing, assembling and mailing the Notice of AnnualSpecial Meeting of Shareholders, this Proxy Statement,proxy statement, the enclosed form of proxy and any additional materials, as well as the cost of forwarding solicitation materials to the beneficial owners of stock and all other costs of solicitation.

In anticipation of the need to utilize a proxy solicitation firm to aid in solicitation of Proxies from its shareholders, Daybreak has retained Alliance Advisors to assist in the solicitation of the return of proxies, and will be paid customary fees and reimbursed for out-of-pocket expenses. The estimated cost for this service is approximately $8,000.

Record Date, Shareholders Entitled to Vote

The Company has determined May 27, 2010,March 22, 2022 as the record date with respect to the determination of shareholders entitled to vote at the AnnualSpecial Meeting. Daybreak’s outstanding stock includes both common stock and Series A Convertible Preferred stock.only Common Stock. Only shareholders of record of the Company’s common stock and Series A Convertible Preferred stock at the close of business on May 27, 2010March 22, 2022 are entitled to notice of and to vote at the AnnualSpecial Meeting.

Outstanding Shares, Quorum and Voting

As of May 27, 2010,March 22, 2022, the record date, there were 47,785,59967,881,207 shares of Daybreak common stock outstanding and entitled to one vote each at the Annual MeetingSpecial Meeting. Of these, 2,738,705 shares of common stock were issued prior to 2005 and 1,008,565the Company has made multiple attempts over the years but not been able to locate the holders of these shares. We have also made attempts to locate other shareholders with shares issued in 2005 and after, and determined that 2,617,923 shares have bad addresses; meaning they have returned mail and/or insufficient/incomplete mailing addresses on file. Our records show that 14,375 shares have been turned over to various states in accordance with state escheatment laws. As a result of these conditions, 5,371,003 shares will not be voted, and will not be counted in determining the number of shares necessary for a quorum or for shareholder action during this meeting. With this, as of March 22, 2022, the record date, there were 62,510,204 shares of Daybreak Series A Convertible Preferredcommon stock outstanding and entitled to 3,025,595 aggregate votesone vote (“voting shares”) each at the Annual Meeting, which number is equal to the number ofSpecial Meeting. The outstanding voting shares of common stock into which such shares of Series A Convertible Preferred stock could be convertedentitled to vote on the record date. Holders of the common stock and the Series A Convertible Preferred stock vote together as a single class. The outstanding shares of common stockdate were registered in the names of 2,227 shareholders and the outstanding shares of Series A Convertible Preferred stock were registered in the names of 74242 shareholders.

The presence of the holders of a majority of the outstanding shares of the voting powershares of common stock, as determined and Series A Convertible Preferred stock,stated above, either in person or by proxy, is required to constitute a quorum at the AnnualSpecial Meeting.

We will count abstentions and broker non-votes for purposes of determining whether a quorum is

- 2 -

present. Therefore, proxies that are submitted but are not voted FOR or AGAINST (because of abstention, broker non-votes, or otherwise) will be treated as present for all matters considered at the meeting. However, although they are considered in determining the presence of a quorum, abstentions and “broker non-votes” will not be considered “votes cast”. Because abstentions are not counted as votes cast, they will have no effect on any vote, including as to the election of directors. Similarly, broker non-votes will have no effect on the vote.

The stock does not have cumulative voting rights, which means that the holders of more than fifty percent (50%) of the voting power of the shares voting in an election of directors, acting together (as applicable), may elect all of the directors if they choose to do so. In such event, the holders of the remaining shares aggregating less than fifty percent (50%) would not be able to elect any directors. Each common shareholder has the right to vote in

-3-

person or by proxy one vote for every share of stock standing in his or her name on the books of the Company on the record date,date.

Proposal Numbers 1 and each holder2 require a vote of Series A Convertible Preferred stock hastwo-thirds (66 2/3%) of the rightvotes of the voting shares eligible to vote in person or by proxyorder to pass. If Proposal Numbers 1 and 2 are not approved, we will be unable to consummate the numberEquity Exchange.

Proposal Number 3– Election of shares of common stock into which such shares of Series A Convertible Preferred stock could be converted.

Directors - will be elected by a plurality of votes cast. “Plurality”“Plurality” means that the individuals who receive the largest number of votes cast are elected as directors up to the maximum number of directors to be chosen at the meeting. Consequently, withholding authority to vote for a director nominee and broker non-votes in the election of directors will not affect the outcome of the election of directors, except to the extent that the failure to vote for an individual results in another individual receiving a larger number of votes. The election of directors will be accomplished by determining the sixfour nominees receiving the highest total votes. However, if Proposal Numbers 1 and 2 are not also approved, director nominee Darren Williams will not join the board even if he receives enough votes, because his election is not effective unless the Equity Exchange is completed. Further, if Darren Williams is not elected, we will be unable to consummate the Equity Exchange.

All other proposals

Proposal Numbers 4 through 7 will be decided by a majority vote of the votes cast with respect thereto. Although they are considered in determining the presence of a quorum, abstentions and “broker non-votes” will not be considered “votes cast.” Because abstentions are not counted as votes cast, they will have no effect on any vote, including as to the election of directors. Similarly, broker non-votes will have no effect on the vote.

Karol L. Adams and Thomas C. Kilbourne will vote all forms of proxy that are properly completed, signed and returned prior to the AnnualSpecial Meeting in accordance with the instructions indicated thereon, and in their discretion as to any other matters that may properly come before the meeting.

Broadridge Financial Solutions, Inc.,

Issuer Direct, an independent third party, will tabulate and certify the vote, and will have a representative in attendance, by phone, to act as the independent inspector of elections for the AnnualSpecial Meeting.

Most shareholders have a choice of voting on the Internet, by telephone, or by mail using a traditional proxy card. Please refer to the proxy card or other voting instructions included with these proxy materials for information on the voting methods available to you. If you vote by telephone or on the Internet, you do not need to return your proxy card.

Your telephone or Internet vote authorizes the named proxies to vote your shares in the same manner as if you had returned your proxy card. We encourage you to use these cost effective and convenient ways of voting, 24 hours a day, 7 days a week.

Telephone voting is available for residents of the U.S. and Canada.

You can vote by calling the toll-free telephone number on your proxy card or by visiting the Internet voting website. Please have your proxy card in hand when you call. Easy-to-follow voice prompts allow you to vote your shares and confirm that your instructions have been properly recorded. Telephone voting is only available for residents of the U.S. and Canada.

Telephone and Internet voting facilities for shareholders of record will be available 24 hours a day, and will close at 11:59 PM Eastern Time on July 21, 2010.May 19, 2022.

The

If you provide specific voting instructions, your shares will be voted as you instruct.

For Beneficial Owners who hold their shares through a broker, bank or other financial institution, the availability of telephone and Internet voting for beneficial owners will depend on the voting processes of your broker, bank or other holder of record. Therefore, we recommend that you follow the voting instructions in the materials you receive.

If you provide specific voting instructions, your shares will be voted as you instruct. If you hold your shares directly

Broker Discretionary Voting and sign the proxy card but do not provide instructions, or if you do not make specific Internet or telephone voting choices, your shares will be voted “FOR” the electionEffect of all director nominees, and “FOR” the ratification of the appointment of MaloneBailey, LLP (“MaloneBailey”), as our independent registered public accountants for the year ending February 28, 2011.Abstentions

- 3 -

If you hold your shares through a broker, bank or other financial institution, the SEC has approved a New York Stock Exchange (“NYSE”) rule that changes the manner in which your vote in the election of directors will be handled at our upcoming 2010 Annual Meeting.

Effective January 1, 2010, if you hold your shares through a broker, bank or other financial institution, your broker will no longernot be permitted to vote on Proposals 1 through 6 on your behalf on the election of directors unless you provide specific instructions by completing and returning the proxy card or following the instructions provided to you to vote your shares via telephone or the Internet. For your vote to be counted, you will now need to communicate your voting decisions to your broker, bank or other financial institution before the date of the shareholder meeting.

-4-

If you sign the proxy card of your broker, trustee, or other nominee, but do not provide instructions, or if you do not make specific Internet or telephone voting choices, your shares will not be voted unless your broker, trustee,on Proposals 1 through 5 or other nominee has discretionary authority to vote.Proposal 7. When a broker, trustee, or other nominee holding shares for a beneficial owner does not vote on a particular proposal because the broker does not have authority to vote in the absence of timely instructions from the beneficial owner, this is referred to as a “broker non-vote.” Brokers who are members of the NYSE have discretionary authority to vote the shares of a beneficial owner in the ratification of MaloneBailey as our independent registered public accountants, but such brokers aremay not empowered to vote for the election of directors in the absence of specific instructions from the beneficial owner.

If you complete and submit your proxy, the shares represented by your proxy will be voted at the Annual Meeting in accordance with your instructions. If you submit a properly executed a proxy but you do not fill out the voting instructions on the proxy card, the shares represented by your proxy will be voted as follows:

|

|

|

|

In addition, if other matters come before the Annual Meeting, the persons named as proxies have discretionary authority to vote on those mattersany Proposals except Proposal Number 6.

An “abstention” occurs when a shareholder sends in accordance with their best judgment.a proxy by mail, telephone or the internet, but does not provide specific voting instructions, fails to cast a ballot or declines to vote regarding a particular matter or attends the Special Meeting and elects not to vote or fails to cast a ballot. Abstentions are treated as shares present in person or by proxy and entitled to vote.

Although the Company will include abstentions and broker non-votes as present or represented for purposes of establishing a quorum for the transaction of business, for Proposals 1 and 2, which require approval of two-thirds of all shares eligible to vote, abstentions and broker non-votes will have the effect of a “NO” vote. The Board is not currently awareCompany intends to exclude abstentions and broker non-votes from the tabulation of any other matters to come before the meeting.

We intend to announce preliminary voting results atfor Proposals 3 – 7, which require approval of a majority of the Annual Meeting and publish final results in a Current Report on Form 8-K within four business days following the Annual Meeting.votes cast.

You have the right to revoke your proxy at anytimeany time prior to its exercise by written notice to the Corporate Secretary at: Daybreak Oil and Gas, Inc., 601 W. Main Avenue,1101 N. Argonne Rd., Suite 1012,A 211, Spokane Washington 99201.Valley, WA 99212. Your written revocation will be effective only if the Corporate Secretary receives the notice at least twenty-four (24) hours prior to the AnnualSpecial Meeting, or if the Inspector of Election receives the notice at the AnnualSpecial Meeting.

AnnualSpecial Meeting Attendance

Subject to space availability, all shareholders as of the record date, or their duly appointed proxies, may attend the AnnualSpecial Meeting, and each may be accompanied by one guest. Admission to the AnnualSpecial Meeting will be on a first-come, first-served basis. Registration will begin at 9:30 AM (PDT)a.m. and the AnnualSpecial Meeting will begin at 10:00 AM (PDT).a.m., local time. Please note that we may ask you to present valid identification when you check in at the registration desk.

If you hold your shares in “street name” (that is, through a broker or other nominee), you will need to bring a copy of a brokerage statement reflecting your stock ownership as of the record date.

You may not bring cameras, recording equipment, electronic devices, large bags, briefcases or packages into the AnnualSpecial Meeting.

- 4 -

We intend to announce preliminary voting results at the Special Meeting and publish final results in a Current Report on Form 8-K within four business days following the Special Meeting.

Proxy Statement Mailing Information;

Delivery of Documents to Security Holders Sharing an Address; Householding

The SEC rules permit companies and intermediaries, such as brokers and banks, to satisfy delivery requirements for proxy statements with respect to two or more shareholders sharing the same address, by delivering a single proxy statement, letter to shareholders from our President and Chief Executive Officer, and annual report on Form 10-K to those shareholders. This method of delivery, often referred to as “householding” is meant to reduce both the amount of duplicate information that shareholders receive and printing and mailing costs. To take advantage of this opportunity, the Company delivers only one proxy statement, letter to shareholders from our President and Chief Executive Officer, and annual report on Form 10-K to multiple shareholders who share an address. If you prefer to receive separate copies of a proxy statement, letter to shareholders from our President and Chief Executive Officer, or annual report on Form 10-K, either now or in the future, or if you currently are a shareholder sharing an address with another shareholder and wish to receive only one copy of future proxy materials for your household, please send your request in writing to the Company at the following address: 601 W. Main Avenue,1101 N. Argonne Rd., Suite 1012,A 211, Spokane Washington 99201,Valley, WA 99212, Attn: Corporate Secretary or call (509) 232-7674.

-5-

We are mailing this Proxy Statementproxy statement and the accompanying Notice of AnnualSpecial Meeting of Shareholders and form of proxy to our shareholders on or about June 11, 2010.April 21, 2022.

Access to Corporate Governance Documents and Annual Reports on Form 10-K

Our Corporate Governance policies and procedures are available under the “Shareholder/FinancialFinancial” - Corporate“Corporate Governance” section of our website at www.daybreakoilandgas.comand are also available upon request, without charge, by contacting the Corporate Secretary at Daybreak Oil and Gas, Inc., 601 W. Main Avenue,1101 N. Argonne Rd., Suite 1012, A 211,

Spokane Washington 99201.Valley, WA 99212. The contents of this website are not incorporated by reference and the website address provided in this Proxy Statementproxy statement is intended to be an inactive textual reference only.

We refer you to our Annual Report on Form 10-K for the fiscal year ended February 28, 2010,2021, which includes our audited financial statements; however, that report does not form anyapplicable provisions of our Annual Report on Form 10-K are hereby incorporated by reference into, and made a part of, the material for the solicitation of proxies.this proxy statement.

The Annual Report on Form 10-K is available under the “Shareholder/Financial – Annual and Quarterly Reports” section of our website at www.daybreakoilandgas.comand is also available upon request, without charge, by contacting the Corporate Secretary at Daybreak Oil and Gas, Inc., 601 W. Main Avenue,1101 N. Argonne Rd., Suite 1012,A 211, Spokane Valley, WA 99212.

| -6- |

SUMMARY OF THE EXCHANGE TRANSACTION AND THE RELATED TRANSACTIONS

The following is a summary of the material terms of the Exchange Agreement. Please see below under “Proposal Number 1” for a more detailed discussion.

On October 20, 2021, and subsequently amended on February 22, 2022, Daybreak entered into an Equity Exchange Agreement (as amended, the “Exchange Agreement”) by and between Daybreak, Reabold California LLC, a California limited liability company (“Reabold”), and Gaelic Resources Ltd., a private company incorporated in the Isle of Man and the 100% owner of Reabold (“Gaelic”), pursuant to which the parties propose for (i) Daybreak to acquire 100% ownership of Reabold, in exchange for (ii) Daybreak issuing 160,964,489 shares of its common stock, par value $0.001 (“Common Stock”) to Gaelic (the “Exchange Shares”), which will result in Reabold becoming a wholly-owned subsidiary of Daybreak named “Reabold California, LLC” and Gaelic becoming the owner of the Exchange Shares and a major shareholder of Daybreak (the foregoing transaction and the transactions contemplated thereby, the “Equity Exchange”). The Exchange Agreement and subsequent Amendment are described in more detail beginning on page 35, and attached hereto as Annex A.

Following the closing of the Equity Exchange, Daybreak will be appointed the sole manager of “Reabold California, LLC”, the Daybreak Subsidiary.

In connection with the Equity Exchange, and as conditions to closing the Equity Exchange, we also propose to, or are required to:

| (a) | Amend and restate our Amended and Restated Articles of Incorporation to (i) increase the number of total authorized shares of Common Stock to 500,000,000 to provide enough shares to accomplish the transactions contemplated by the Equity Exchange and conducted in anticipation of the Equity Exchange, and other potential future issuances, and (ii) allow a majority share vote to approve transactions where a higher vote is provided by the Washington Business Corporation Act (Proposal; Number 2, see page 38); |

| (b) | Nominate Darren Williams, a nominee selected by Reabold, to the Daybreak Board of Directors, to join the board effective as of the closing of the Equity Exchange (Proposal; Number 3, see page 40); |

| (c) | Enter into a voting agreement by and among Daybreak, Gaelic and the Company’s Chairman and Chief Executive Officer, James F. Westmoreland, where, on the terms therein, Daybreak and the shareholder parties thereto agree to nominate a person designated by Gaelic and a person designated by James F. Westmoreland to Daybreak’s Board of Directors, and the parties thereto agree to vote their shares in favor of such candidates (the “Voting Agreement”). The Voting Agreement is described in more detail beginning on page 69, and attached hereto as Exhibit D to the Exchange Agreement (Annex A); |

| (d) | Enter into agreements to sell a minimum of $2,500,000 of shares of Daybreak’s Common Stock, and a minimum of 125,000,000 shares of Common Stock, to one or more investors in a private placement expected to close promptly following the closing of the Equity Exchange (the “Capital Raise”), with the proceeds of the Capital Raise to be used to repay in full the Company’s line of credit with UBS Bank and for drilling and exploration activities and other working capital purposes; |

| (e) | Enter into a registration rights agreement between Daybreak and the purchasers of common stock pursuant to the Capital Raise giving such purchasers rights to demand or participate in registration of Common Stock held by them on the terms contained therein; |

| (f) | Effective upon the closing of the Equity Exchange, appoint Integrity Management Solutions, Inc. (“Integrity”), a California operating company that provides engineering and contract operating services for Reabold California LLC’s oil and gas properties. Integrity has been providing these services for the Reabold properties since July, 2018, as contract operator of Reabold’s oil and gas license interests for a minimum of a one (1) year period; and |

-7-

| (g) | Effective upon the closing of the Equity Exchange, enter into indemnification agreements between Company and its directors. |

Also, in connection with the Equity Exchange, and as conditions to closing the Equity Exchange, we have already taken the following steps to simplify the Company’s share structure and eliminate indebtedness:

| (h) | Converted all shares of Series A Preferred Stock of the Company to Common Stock by approval of the holders of a majority of the shares of Series A Preferred Stock (the “Series A Conversion”); |

| (i) | Converted $1,837,101 of related party liabilities of Daybreak into Common Stock of the Company (the “Related Party Debt Conversion”), including all accrued and unpaid salary and fees of our named executive officers, certain other employees and directors. |

| (j) | The Company’s President and Chief Executive Officer forgave $43,192 in deferred salary payments, net of related taxes and expense reimbursements. |

On February 22, 2022 the Equity Exchange Agreement was amended, effective as of February 14, 2022, to (1) allow Daybreak to sell a convertible promissory note to a Private Investor in the amount of US$200,000; (2) extend the Long Stop Date to April 29, 2022; (3) Allow Reabold California LLC to borrow up to $250,000 from Reabold Resources PLC to conduct certain operational activities necessary to maintain the production of oil and gas on its leases. This money will be paid back to Reabold Resources PLC upon the closing of the Equity Exchange Agreement; and (4) Daybreak agreed to compensate Gaelic in the form of a breakage fee of US$500,000 in Daybreak common stock if the Equity Exchange is not closed by April 29, 2022.

Reabold California LLC, a California limited liability company (“Reabold”), is an oil and gas exploration and production company based in California located at 5701 Lonetree Blvd., Rocklin, CA 95765, and can be reached by phone number at 916-872-1833.

Reabold invests in the exploration and production sector of the energy industry. Its investing policy is to acquire direct and indirect interests in exploration and producing projects and assets in the natural resources sector. As an investor in upstream oil and gas projects, Reabold aims to create value from each asset by investing in undervalued, low-risk, upstream oil and gas opportunities with near-term activity and by identifying potential monetization plans prior to investment.

Reabold invests in projects that have limited correlation to the oil price. They believe the value realization of a project is determined by monetizing the asset (putting it into production or selling it); and the value increase of an asset from the acquisition entry point to monetization is achieved through successful appraisal and/or development drilling.

A brief description of the transaction. If approved, upon the closing of the Equity Exchange, (i) Daybreak will acquire 100% ownership of Reabold, in exchange for (ii) Daybreak issuing 160,964,489 shares of its Common Stock (the “Exchange Shares”) to Reabold’s owner, Gaelic, which will result in Reabold becoming a wholly-owned subsidiary of Daybreak named “Reabold California, LLC” and Gaelic becoming the owner of the Exchange Shares and a major shareholder of Daybreak (the foregoing transaction and the transactions contemplated thereby, the “Equity Exchange).

Consideration offered to security holders. The only consideration being offered in connection with the Equity Exchange is assignment of membership interests of Reabold from Gaelic to Daybreak, and the issuance of the Exchange Shares from Daybreak to Gaelic. The existing shareholders of Daybreak will not receive any consideration.

The reasons for engaging in the transaction. Daybreak proposes to complete the Equity Exchange as part of a larger reorganization of the Company as described herein. Daybreak has faced the challenges of declining oil prices (historically) and the lack of outside financing for several years. We have been working steadily to minimize overhead and unnecessary expenditures, simplify our share structure, and position the Company for a strategic

| -8- |

turnaround transaction. The Company has already converted certain related party debt, certain of the Company’s 12% subordinated notes and the Company’s Series A preferred stock into Common Stock to achieve this goal. Completing the Equity Exchange and the Capital Raise are the next two important steps in the Company’s growth strategy.

The vote required for approval of the transaction. Pursuant to Section 23B.11.030 of the Washington 99201.Business Corporation Act, to be approved, the Equity Exchange must be approved by Daybreak shareholders by a vote of two thirds (66 2/3%) of all votes entitled to be cast, or two-thirds of all outstanding shares of Common Stock entitled to vote. Gaelic, Reabold’s sole shareholder, has approved the transaction on behalf of Gaelic.

An explanation of any material differences in the rights of security holders as a result of the transaction, if material.The Equity Exchange and the transactions contemplated thereby will dilute the overall percentage ownership of each existing shareholders pro rata to the number of shares owned. However, we believe the transactions, including the proposed authorization of additional shares of Common Stock to issue in the Equity Exchange, will increase the value of the Company and ultimately build shareholder value for all shareholders, including existing shareholders.

A brief statement as to the accounting treatment of the transaction. There are no material considerations to our shareholders associated with the accounting treatment of the Equity Exchange.

The federal income tax consequences of the transaction. The Equity Exchange is expected to be a tax-free transaction. There should not be any tax effect to our existing shareholders as a result of the Equity Exchange.

Additional Financial Considerations Related to the Equity Exchange Agreement

Pursuant to the amendment to the Equity Exchange Agreement entered into on February 22, 2022 (the “Exchange Agreement Amendment”), Daybreak and Gaelic agreed to allow Reabold to borrow up to $250,000 from Gaelic’s parent company, Reabold Resources PLC, to conduct certain operational activities necessary to maintain the production of oil and gas on its leases, to be paid back to Reabold Resources PLC by Daybreak upon the closing of the Equity Exchange Agreement.

Also pursuant to the Exchange Agreement Amendment, Daybreak agreed to issue to Gaelic shares of Daybreak common stock worth US$500,000 if the Equity Exchange is not closed by April 29, 2022 (the “Break Fee Shares”), priced according to the average price calculated over the five trading days prior to and including the Long-Stop Date, with payment (to be satisfied by the issuance of the Break Fee Shares) made as soon as practicably possible after the amended Long-Stop Date has expired. However, if the Equity Exchange Agreement is completed after an agreed upon date after April 29, 2022, then 50% of the Break Fee Shares issued to Gaelic will be applied in part satisfaction of the number of the Parent Shares that are due to Gaelic under the Exchange Agreement; and

On or about February 22, 2022, Company issued a convertible promissory note to a private investor (the “purchaser”) in the amount of US$200,000 (the “Convertible Note”). The Convertible Note will convert into shares of the Company’s common stock upon the earlier of the closing of the Equity Exchange Agreement or the purchaser’s instruction any time on or after April 29, 2022. If the closing of the Equity Exchange Agreement is on or before April 29, 2022, the Convertible Note will convert at a price of $0.017 per share, into approximately 13,882,353 common shares, including payable-in-kind interest. If the Convertible Note converts after April 29, 2022, it will convert at a price of $0.0085 per share, into approximately 27,764,706 common shares, including payable-in-kind interest. Payable-in-kind interest accrues on the Convertible Note at a rate of 18% per annum with a minimum of one year of interest payable. The terms of the Convertible Note also provide that if the Company sells shares over the next six months for a price less than $0.02 per share, the Company will adjust the number of conversion shares issued under the Convertible Note accordingly, at a conversion price equal to the sale price with a 15% discount.

Therefore, if the Equity Exchange Agreement is not closed by April 29, 2022, the existing shareholders will experience additional significant dilution.

-9-

There are no federal or state regulatory requirements that must be complied with, or approvals that must be obtained from federal or state regulatory officials, in connection with the Equity Exchange and the transactions contemplated thereby.

The parties to the Equity Exchange have not obtained any reports, opinions or appraisals from any outside parties materially relating to the Equity Exchange.

Past Contacts, Transactions or Negotiations

Other than the negotiations with respect to the Equity Exchange, there have been no other transactions or material contacts during the past two years between Daybreak or any of its affiliates and Reabold or any of its affiliates concerning any merger, consolidation, acquisition, tender offer, election of directors, or sale or other transfer of a material amount of assets of Reabold or Daybreak.

Appraisal Rights and Dissenters’ Rights

Holders of Daybreak Common Stock are not entitled to appraisal or dissenters’ rights in connection with the Equity Exchange.

Interests of Certain Persons in the Equity Exchange

In considering the recommendation of the Daybreak Board of Directors with respect to the approval of the Equity Exchange and the transactions contemplated by the Exchange Agreement, and the other matters to be acted upon by the Daybreak shareholders at the Special Meeting, the Daybreak shareholders should be aware of the following potential conflict of interest: if the Equity Exchange is approved, Daybreak, Gaelic and Daybreak’s Chairman and Chief Executive Officer, James F. Westmoreland, will enter into the Voting Agreement, where, on the terms therein, Daybreak and the parties thereto agree to nominate a person designated by Gaelic (Darren Williams) and a person designated by James F. Westmoreland (James F. Westmoreland) to Daybreak’s Board of Directors, and the parties thereto agree to vote their shares in favor of such candidates.

The Board of Directors of Daybreak was aware of these potential conflicts of interest and considered it, among other matters, in reaching its decision to approve the Equity Exchange, and to recommend that the Daybreak shareholders approve the proposals to be presented to them for consideration at the Special Meeting as contemplated by this proxy statement.

There are no agreements between any named executive officer and the Company, Gaelic, or Reabold concerning any type of compensation, whether present, deferred or contingent, that is based on or otherwise relates to the completion of the Equity Exchange.

FINANCIAL INFORMATION AND BACKGROUND ABOUT THE PARTIES

For more information about Daybreak, we refer you to our Annual Report on Form 10-K for the fiscal year ended February 28, 2021, which includes our audited financial statements; applicable provisions of our Annual Report on Form 10-K are hereby incorporated by reference into, and made a part of, this proxy statement.

Organizational History

Reabold California, LLC, a California limited liability company (“referred to in this Section as “we,” “our,” “us,” or “Reabold” or the “Company”), is a wholly owned subsidiary of Gaelic Resources Ltd. (“Gaelic”), a private company incorporated in the Isle of Man, a self-governing British Crown dependency. Gaelic is a wholly owned subsidiary of Reabold Resources Plc (“RBD Plc”), a company incorporated in the United Kingdom and listed on the Alternative Investment Market of the London Stock Exchange. Our operating and financial results are included in the public filings by RBD Plc of consolidated financial reporting in the United Kingdom.

-10-

Business Description

Overview

We invest in the exploration and production sector of the energy industry. Our investing policy is to acquire direct and indirect interests in exploration and producing projects and assets in the natural resources sector. As an investor in upstream oil and gas projects, we aim to create value from each asset by investing in undervalued, low-risk, upstream oil and gas opportunities with near-term activity and by identifying potential monetization plans prior to investment.

We invest in projects that have limited correlation to the oil price. The value realization of a project is determined by monetizing the asset (putting it into production or selling it). The value increase of an asset from the acquisition entry point to monetization is achieved through successful appraisal and/or development drilling.

California Crude Oil and Natural Gas Projects

Our crude oil and natural gas production is located in the Sacramento Basin within Monterey and Contra-Costa Counties in California. Production in Monterey County is from the Monroe Swell area for our three Burnett wells. Production in Contra-Costa County is from the Meganos Unconformity area for our three West Brentwood wells. California is a state with very high renewable energy generation which feeds into the energy required for hydrocarbon extraction. By industry standards, our oil and gas activities require a very low level of energy to extract the hydrocarbons.

Reabold’s interests in US oil and gas leases are operated by Integrity Management Solutions, Inc. (“Integrity”), a California operating company that leads direct operational decisions pertaining to these leases, in consultation with Reabold management to ensure high standards of conduct in line with Reabold’s policies. Integrity has been providing these services for the Reabold properties since July, 2018. Integrity led a successful five well drilling program in 2018 and 2019. Two of these wells the Burnett 2A and 2B are located in the Monroe Swell Field, the other three wells, the VG-3, VG-4 and VG-6 are located in the West Brentwood Field. We completed the fifth well of that program, the VG-6, in February 2020. Since that time we have been concentrating our efforts on reducing the operating expenses of our three VG wells through the successful permitting of a disposal/injection well permit to dispose of our produced water.

Our California assets are characterized by relatively low cash operating costs and continued to be cash generative amidst the lower oil and gas price environment that was experienced during much of 2020. With the significant increase in oil prices in 2021 crude oil revenues increased while operating profit was offset by lower production due to workover of wells and bringing enhanced storage infrastructure online. Operating costs per barrel in 2020 and 2021 were negatively impacted by significantly increased water disposal costs, which will be reduced when the water disposal wells are brought online in 2022.

California Reserves

Our total crude oil and natural gas reserves as of April 1, 2021, were comprised of our 50% working interest in the Monroe Swell and West Brentwood Fields. Pricing is based on New York Mercantile Exchange (“NYMEX”) Brent as published by CME Group and are subject to the usual adjustments for quality, transportation fees, market differentials and other local conditions.

| Proved Reserves | ||||||||||||||||

| Reserve Category | Crude Oil (Barrels) | Natural Gas (Mcf) (1) | Total Crude Oil Equivalents (BOE) | Percent of Oil Equivalents (BOE) | ||||||||||||

| Developed | 285,360 | 36,790 | 291,492 | 47.6 | % | |||||||||||

| Undeveloped | 321,500 | — | 321,500 | 52.4 | % | |||||||||||

| Total Proved | 606,860 | 36,790 | 612,992 | 100.0 | % | |||||||||||

(1) One barrel of crude oil equivalent (“BOE”) is roughly equivalent to 6,000 cubic feet or 6 Mcf of gas

Our estimated proved reserves (BOE) and PV-10 valuation in California at April 1, 2021 are set forth in the table below.

| Proved Reserves | ||||||||||

| PV-10 as a | ||||||||||

| Total Oil | PV-10 of | Percentage of | ||||||||

| Locations | Equivalents (BOE) (1) | Proved Reserves | Proved Reserves | |||||||

| Monroe Swell and West Brentwood Fields, California | 612,992 | $ | 12,944,960 | 100.0 | % | |||||

(1) One barrel of crude oil equivalent (“BOE”) is roughly equivalent to 6,000 cubic feet or 6 Mcf of gas

| -11- |

Financial Information

The financial statements shown below for Reabold are derived from the audited consolidated financial statements of RBD Plc for the years ended December 31, 2019 and 2020 and the unaudited financial statements of Reabold for the twelve months ended December 31, 2019 and 2020.

Reabold California, LLC

Balance Sheets - 5Unaudited

As of December 31, 2020 | As of December 31, 2019 | |||||||

| ASSETS | ||||||||

| CURRENT ASSETS: | ||||||||

| Cash and cash equivalents | $ | 107,000 | $ | 43,000 | ||||

| Restricted cash | 250,000 | 450,000 | ||||||

| Trade and other receivables | 174,000 | 823,000 | ||||||

| Inventory | 46,000 | 26,000 | ||||||

| Total current assets | 577,000 | 1,342,000 | ||||||

| LONG TERM ASSETS | ||||||||

| Oil and gas properties | 1,583,000 | 2,079,000 | ||||||

| Property, plant and equipment | 6,236,000 | 5,812,000 | ||||||

| Total long-term assets | 7,819,000 | 7,891,000 | ||||||

| Total assets | $ | 8,396,000 | $ | 9,223,000 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| CURRENT LIABILITIES: | ||||||||

| Trade and other payables | $ | 250,000 | $ | 1,090,000 | ||||

| Notes payable - related parties | 8,587,000 | 7,964,000 | ||||||

| Accrued liabilities | — | 85,000 | ||||||

| Total current liabilities | 8,837,000 | 9,139,000 | ||||||

| LONG TERM LIABILITIES: | ||||||||

| Asset retirement obligation | 52,000 | 89,000 | ||||||

| Total long-term liabilities | 52,000 | 89,000 | ||||||

| Total liabilities | 8,889,000 | 9,228,000 | ||||||

| COMMITMENTS AND CONTINGENCIES | ||||||||

| STOCKHOLDERS’ EQUITY: | ||||||||

| Common stock | 1,000 | 1,000 | ||||||

| Accumulated deficit | (494,000 | ) | 4,000 | |||||

| Total stockholders’ equity | (493,000 | ) | 5,000 | |||||

| Total liabilities and stockholders' equity | $ | 8,147,000 | $ | 9,223,000 | ||||

| -12- |

Reabold California, LLC

Statements of Operations - Unaudited

Twelve Months Ended December 31, 2020 | Twelve Months Ended December 31, 2019 | |||||||

| REVENUE: | ||||||||

| Crude oil and natural gas sales | $ | 1,063,000 | $ | 1,483,000 | ||||

| OPERATING EXPENSES: | ||||||||

| Production | 639,000 | 425,000 | ||||||

| Exploration and drilling | — | 245,000 | ||||||

| Depreciation, depletion and amortization | 418,000 | 298,000 | ||||||

| Impairment | 307,000 | 205,000 | ||||||

| General and administrative | 149,000 | 136,000 | ||||||

| Total operating expenses | 1,513,000 | 1,309,000 | ||||||

| OPERATING LOSS | (450,000 | ) | 174,000 | |||||

| OTHER EXPENSE: | ||||||||

| Interest expense, net | (48,000 | ) | (183,000 | ) | ||||

| NET LOSS | $ | (498,000 | ) | $ | (9,000 | ) | ||

Reabold California, LLC

Statements of Cash Flows - Unaudited

| Twelve Months Ended | ||||||||

December 31, 2020 | December 31, 2019 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net loss | $ | (498,000 | ) | $ | (9,000 | ) | ||

| Adjustments to reconcile net loss to net cash provided by (used in) operating activities: | ||||||||

| Capitalized costs expensed to exploration | — | 245,000 | ||||||

| Depreciation, depletion and amortization | 418,000 | 298,000 | ||||||

| Impairment | 307,000 | 205,000 | ||||||

| Changes in assets and liabilities: | ||||||||

| Accounts receivable | 649,000 | (436,000 | ) | |||||

| Inventory | (20,000 | ) | 15,000 | |||||

| Accounts payable | (926,000 | ) | 607,000 | |||||

| Provisions | (37,000 | ) | 89,000 | |||||

| Net cash provided by (used in) operating activities | (107,000 | ) | 1,014,000 | |||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Additions to crude oil and natural gas properties | (142,000 | ) | (880,000 | ) | ||||

| Additions to property, plant and equipment | (511,000 | ) | (4,349,000 | ) | ||||

| Changes in restricted cash | 200,000 | (225,000 | ) | |||||

| Net cash used in investing activities | (453,000 | ) | (5,454,000 | ) | ||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Proceeds on notes payable – related party | 624,000 | 3,250,000 | ||||||

| Net cash (used in) provided by financing activities | 624,000 | 3,250,000 | ||||||

| NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | 64,000 | (1,190,000 | ) | |||||

| CASH AND CASH EQUIVALENTS AT BEGINNING OF PERIOD | 43,000 | 1,233,000 | ||||||

| CASH AND CASH EQUIVALENTS AT END OF PERIOD | $ | 107,000 | $ | 43,000 | ||||

| -13- |

The financial statements shown below for Reabold are derived from the audited consolidated financial statements of RBD Plc for the year ended December 31, 2020 and the unaudited financial statements of Reabold for the twelve months ended December 31, 2020 and the eleven months ended November 30, 2021.

Reabold California, LLC

Balance Sheets - Unaudited

As of November 30, 2021 | As of December 31, 2020 | |||||||

| ASSETS | ||||||||

| CURRENT ASSETS: | ||||||||

| Cash and cash equivalents | $ | 292,000 | $ | 107,000 | ||||

| Restricted cash | 250,000 | 250,000 | ||||||

| Trade and other receivables | 55,000 | 174,000 | ||||||

| Inventory | 29,000 | 46,000 | ||||||

| Total current assets | 626,000 | 577,000 | ||||||

| LONG TERM ASSETS | ||||||||

| Oil and gas properties | 1,697,000 | 1,583,000 | ||||||

| Property, plant and equipment | 5,824,000 | 6.236,000 | ||||||

| Total long-term assets | 7,521,000 | 7,819,000 | ||||||

| Total assets | $ | 8,147,000 | $ | 8,396,000 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| CURRENT LIABILITIES: | ||||||||

| Trade and other payables | $ | 232,000 | $ | 250,000 | ||||

| Notes payable - related parties | 6,449,000 | 8,587,000 | ||||||

| Total current liabilities | 6,681,000 | 8,837,000 | ||||||

| LONG TERM LIABILITIES: | ||||||||

| Asset retirement obligation | 54,000 | 52,000 | ||||||

| Total long-term liabilities | 54,000 | 52,000 | ||||||

| Total liabilities | 6,735,000 | 8,889,000 | ||||||

| COMMITMENTS AND CONTINGENCIES | ||||||||

| STOCKHOLDERS’ EQUITY: | ||||||||

| Common stock | 2,205,000 | 1,000 | ||||||

| Accumulated deficit | (793,000 | ) | (494,000 | ) | ||||

| Total stockholders’ equity | 1,412,000 | (493,000 | ) | |||||

| Total liabilities and stockholders' equity | $ | 8,147,000 | $ | 8,396,000 | ||||

| -14- |

Reabold California, LLC

Statements of Operations - Unaudited

Nine Months Ended November 30, 2021 | Nine Months Ended November 30, 2020 | |||||||

| REVENUE: | ||||||||

| Crude oil and natural gas sales | $ | 1,013,000 | $ | 655,000 | ||||

| OPERATING EXPENSES: | ||||||||

| Production | 776,000 | 485,000 | ||||||

| Depreciation, depletion and amortization | 389,000 | 308,000 | ||||||

| General and administrative | 97,000 | 142,000 | ||||||

| Total operating expenses | 1,262,000 | 935,000 | ||||||

| OPERATING LOSS | (249,000 | ) | (280,000 | ) | ||||

| OTHER EXPENSE: | ||||||||

| Interest expense, net | (10,000 | ) | (25,000 | ) | ||||

| NET LOSS | $ | (259,000 | ) | $ | (305,000 | ) | ||

Reabold California, LLC

Statements of Cash Flows - Unaudited

| Nine Months Ended | ||||||||

November 30, 2021 | November 30, 2020 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net loss | $ | (259,000 | ) | $ | (305,000 | ) | ||

| Adjustments to reconcile net loss to net cash provided by (used in) operating activities: | ||||||||

| Depreciation, depletion and amortization | 389,000 | 308,000 | ||||||

| Changes in assets and liabilities: | ||||||||

| Accounts receivable | 85,000 | 668,000 | ||||||

| Inventory | 17,000 | 2,000 | ||||||

| Accounts payable | 8,000 | (916,000 | ) | |||||

| Provisions | — | (39,000 | ) | |||||

| Net cash provided by (used in) operating activities | 240,000 | (282,000 | ) | |||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Additions to crude oil and natural gas properties | (80,000 | ) | (222,000 | ) | ||||

| Additions to property, plant and equipment | (22,000 | ) | (346,000 | ) | ||||

| Changes in restricted cash | — | 200,000 | ||||||

| Net cash used in investing activities | (102,000 | ) | (368,000 | ) | ||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Proceeds on notes payable – related party | 64,000 | 617,000 | ||||||

| Net cash (used in) provided by financing activities | 64,000 | 617,000 | ||||||

| NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | 202,000 | (33,000 | ) | |||||

| CASH AND CASH EQUIVALENTS AT BEGINNING OF PERIOD | 90,000 | 18,000 | ||||||

| CASH AND CASH EQUIVALENTS AT END OF PERIOD | $ | 292,000 | $ | (15,000 | ) | |||

| -15- |

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Safe Harbor Provision

Certain statements contained in Reabold’s Management’s Discussion and Analysis of Financial Condition and Results of Operations are intended to be covered by the safe harbor provided for under Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Exchange Act. All statements other than statements of historical facts contained in this MD&A report, including statements regarding Reabold’s current expectations and projections about future results, intentions, plans and beliefs, business strategy, performance, prospects and opportunities, are inherently uncertain and are forward-looking statements.

Results of Operations – For the Years ended December 31, 2020 and 2019

California Crude Oil and Natural Gas Prices

Our crude oil and natural gas pricing is based on New York Mercantile Exchange (“NYMEX”) Brent as published by CME Group and are subject to the usual adjustments for quality, transportation fees, market differentials and other local conditions.

The price we receive for natural gas sales in California is based on published pricing in the Natural Gas Intelligence, Gas Price Index – Bidweek Averages for “California”, “PG&E Citygate” of 95%, less deductions for transport rates and transmission shrinkage.

It is beyond our ability to accurately predict the level at which crude oil and natural gas prices will remain or when and at what level they may stabilize.

California Crude Oil and Natural Gas Revenue

Crude oil and natural gas revenue in California for the twelve months ended December 31, 2020 decreased $420,000 or 28.3% to $1,063,000 in comparison to revenue of $1,483,000 for the twelve months ended December 31, 2019. The average sale price of a barrel of crude oil equivalent (BOE)(1)(2) for the twelve months ended December 31, 2021 was $38.40 in comparison to $60.00 for the twelve months ended December 31, 2019.

| (1) | One barrel of crude oil equivalent (“BOE”) is roughly equivalent to 6,000 cubic feet or 6 Mcf of gas |

| (2) | Net average sales price before royalties of 20% |

Our crude oil net sales volume for the twelve months ended December 31, 2020 was 31,728 barrels of crude oil in comparison to 29,345 barrels sold for the twelve months ended December 31, 2019. Reabold’s natural gas net sales volume for the twelve months ended December 31, 2020 was 17,129 Mcf in comparison to 9,219 Mcf for the twelve months ended December 31, 2019.

Operating Expenses

Total operating expenses for the twelve months ended December 30, 2020 were $1,514,000, an increase of $205,000 or 15.7% compared to $1,309,000 for the twelve months ended December 31, 2019. Operating expenses for the twelve months ended December 30, 2020 and 2019 are set forth in the table below:

Twelve Months Ended December 31, 2020 | Twelve Months Ended December 31, 2019 | |||||||||||||||

| Expenses | Percentage | Expenses | Percentage | |||||||||||||

| Production expenses | $ | 639,000 | 42.2 | % | $ | 425,000 | 32.5 | % | ||||||||

| Exploration expenses | — | 0.0 | % | 245,000 | 18.7 | % | ||||||||||

| Depreciation, depletion and amortization (“DD&A”) | 418,000 | 27.7 | % | 298,000 | 22.7 | % | ||||||||||

| Impairment | 307,000 | 20.3 | % | 205,000 | 15.7 | % | ||||||||||

| General and administrative (“G&A”) expenses | 149,000 | 9.8 | % | 136,000 | 10.4 | % | ||||||||||

| Total operating expenses | $ | 1,513,000 | 100.0 | % | $ | 1,309,000 | 100.0 | % | ||||||||

| -16- |

Results of Operations – For the Nine Months ended November 30, 2021 and 2020

California Crude Oil and Natural Gas Revenue

Crude oil and natural gas revenue in California for the nine months ended November 30, 2021 increased $358,000 or 54.7% to $1,013,000 in comparison to revenue of $655,000 for the nine months ended November 30, 2020.

Operating Expenses

Total operating expenses for the nine months ended November 30, 2021 were $1,262,000, an increase of $327,000 or 35.0% compared to $935,000 for the nine months ended November 30, 2020. Operating expenses for the nine months ended November 30, 2021 and 2020 are set forth in the table below:

Nine Months Ended November 30, 2021 | Nine Months Ended November 30, 2020 | |||||||||||||||

| Expenses | Percentage | Expenses | Percentage | |||||||||||||

| Production expenses | $ | 776,000 | 61.5 | % | $ | 485,000 | 51.9 | % | ||||||||

| Depreciation, depletion and amortization (“DD&A”) | 389,000 | 30.8 | % | 308,000 | 32.9 | % | ||||||||||

| General and administrative (“G&A”) expenses | 97,000 | 7.7 | % | 142,000 | 15.2 | % | ||||||||||

| Total operating expenses | $ | 1,262,000 | 100.0 | % | $ | 935,000 | 100.0 | % | ||||||||

Material Changes in Financial Condition

During the nine months ended November 30, 2021 Reabold experienced an increase in revenues of $358,000 or 54.7% to $1,013,000 in comparison to revenues of $655,000 for the nine months ended November 30, 2020.